June’s auto market saw plugin EVs take 35.9% share in the UK, up from 28.2% year on year. BEVs grew volume 38%, and PHEVs grew 29%. Overall auto volume was 191,316 units, up some 7% YoY. The UK’s leading BEV brand was Tesla, with a 16.1% share of the BEV market.

June’s sales totals saw combined plugin EVs take 35.9% share in the UK, with full electrics (BEVs) taking 24.8% and plugin hybrids (PHEVs) taking 11.2%. These compare with June 2024 shares of 28.2% combined, 19.0% BEV, and 9.3% PHEV.

If we set aside December months – when auto makers often heavily push BEV sales to meet full-year emissions requirements – June’s auto market actually represents a new record high in plugin share (just ahead of November ‘24). This is a good result, and reflects the efficacy of the ZEV mandate scheme that the UK embarked upon starting in 2024.

It also reflects that PHEV share has recently been as strong as ever, thanks to the new generation of PHEVs that can typically drive at least 50 miles in electric-only mode.

Finally, it reflects the fact that the month of June in the UK habitually shows a BEV uptick (check the historical chart below) largely thanks to Tesla making a strong end-of-Q2 push. June 2025 was no exception, with Tesla delivering 7,719 combined units of the Model Y (making it June’s 3rd best-selling vehicle overall) and Model 3 (6th best-selling). This appears to be Tesla’s biggest monthly volume since March 2023.

Meanwhile HEV share was down by some 11% YoY, petrol-only share was down by 3.5%, and diesel-only share was flat. Combined combustion-only share stood at 51.6% and will likely dip below 50% by the end of Q3.

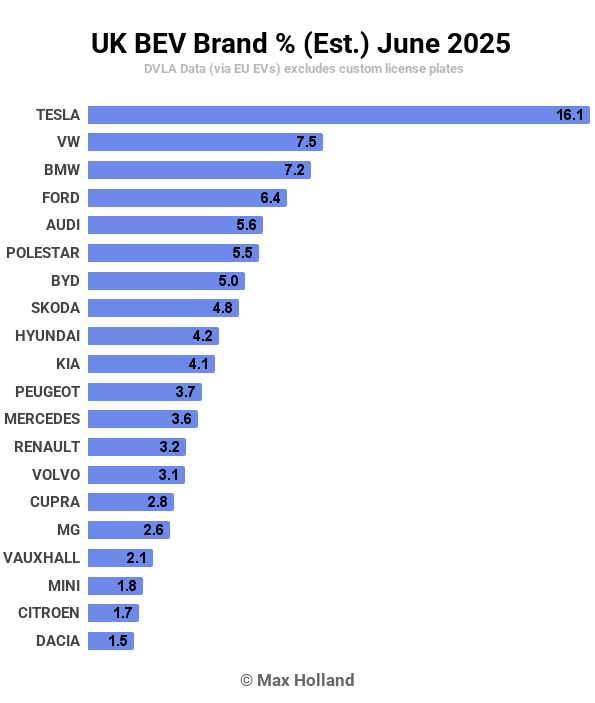

Best-Selling BEV Brands

As noted above, Tesla had a big month in June, and led the BEV brand chart by a wide margin, ahead of the Volkswagen brand, and the BMW brand.

The biggest mover in the monthly rankings was Tesla, up from 4th in May to the top spot in June. Most other changes in ranking were minor shuffles, though further back Polestar also jumped up, from 13th in May to 7th in June.

Outside the top 20, the Alpine brand rose from 37th to 28th, due to first substantial volumes (over 130 units) of its A290 model. Likewise, Xpeng climbed from 40th to 32nd, thanks to over 100 registrations of its G6 SUV, and the first decent volume month in the UK from the innovative brand.

As usual, we don’t have fully accurate data on individual models (with many DVLA registrations listed as “unknown” models), but can pencil out some rough trends. The Skoda Elroq continued to do well, at over 800 units in June, slightly ahead of its May volume, but below its big push in March. For context, the Elroq is still behind its sibling, the Enyaq (one of the top 5 with over 1000 units). It’s also marginally behind the BYD Seal, which saw over 860 units in June.

At the affordable end, the Dacia Spring continued to do well, with 709 units in June, though a bit down from its 766 units in March. Its closest competitor, the Leapmotor T03 saw 77 units in June, barely growing over its 68 units in March (both these import models tend to see peak shipping quarterly). So for now Dacia has the circa-15k price segment well in hand, but more on this below.

Stepping up to the more competent A-B segment models, the Renault 5 stepped up to its highest volume of over 620 units in June (from a little over 500 in May). This means that it leads the segment, ahead of the Hyundai Inster, which saw a decent 448 units in June (from 228 in May). The Renault starts from £22,000 (40 kWh usable), whilst the Hyundai starts from £23,495 (39.0 kWh). Both offer larger battery options for more money.

The other of the “legacy affordable trio”, the Citroën e-C3, was some way down in June with 241 units, below its March peak of 301 units. It’s too early to say whether this is simply a supply limitation, or a demand limitation, but it’s not a great look for the Citroën to be at barely over a third of the Renault 5’s monthly volume, particularly given its slightly earlier UK debut.

Renault is about to pull further ahead, with the Renault 4 just having made its debut in June, with 51 initial units. As we know, the Renault 4 shares the same platform with – though is about 10% larger than – the Renault 5, and has more ground clearance. There’s no sign yet of Citroën’s equivalent, the e-C3 Aircross.

Despite this seeming lead by Renault, there’s now a new kid on the block, in the form of the BYD Dolphin Surf. Having debuted with a modest 11 units in May, the Surf stepped up to a significant 197 units in June. It is therefore already snapping at the heels of the Citroën e-C3.

The Surf is priced starting from £18,650 for the entry (30 kWh) variant. Meanwhile the Citroën e-C3’s entry £21,990 variant comes with a 44 kWh battery. However, the entry e-C3 is still at an almost identical price (per kWh of battery) as the equivalent Dolphin Surf, which is the 43.2 kWh “Boost” variant, with an MSRP of £21,950. So the two are closely aligned once you equalise the basic specs.

If you think this price-alignment is merely a coincidence, it is likely not. One of the EU’s now under-discussion conditions of BYD (and other Chinese brands) doing business in Europe, is to be able to forgo tariffs if they agree to submit to minimum-pricing (i.e. price fixing) to keep European legacy auto makers happy. Price fixing is strictly illegal, but these anti-consumer practices should be no great surprise – I’ve previously reported on legal findings of the cartel behaviour of Europe’s auto makers (including their lobbies, the SMMT and ACEA).

It would be interesting to know the sales split between the two different battery sizes of the BYD Dolphin Surf. The affordable base 30 kWh version has a modest WLTP range of 137 miles, similar to the Dacia Spring, but has much more power and a significantly higher top speed than the Spring (93 mph vs 78 mph), so arguably more suited to highway driving and all-around ability. It also has faster 10-80% DC charging (29 mins vs 38 mins), and a more sophisticated ride, interior, and infotainment than the Spring. These advantages may justify the entry Surf’s higher price than the Spring (£18,650 vs £14,995) for some buyers.

Meanwhile, the Leapmotor T03 (£15,995) has a better WLTP range (165 miles) than either, and similar power to the Surf, though a lower top speed (81 mph) and the slowest DC charging (52 minutes for 10-80%). If you had to choose between one of these three, given their respective prices, which would it be?

At £21,950, the mid-trim 43.2 kWh Surf is an 18% step up in price compared to the base model, but has a more useful WLTP range of 200 miles, the same as the entry Citroën e-C3. There’s even a top-spec surf for £23,950 which adds more power and some interior niceties, though has similar range. Where’s the sweet spot here? I guess it depends on one’s situation, but let us know in the comments.

Anyway, it’s good to see the competition increasing at these relatively affordable price points, and hopefully (unless the EU and legacy auto get their way) more models will quickly join the fray, leading to even better value for consumers.

Here’s the trailing 3-month chart:

Tesla’s big splash in June saw it narrowly retake the lead over the Volkswagen brand. BMW came in third, just ahead of Ford.

This was a relatively good result for Ford, which increased its volumes 22% over Q1 and climbed from 9th to 4th. Likewise, thanks to the new Elroq, Skoda climbed from 11th to 6th, up in volume by 35%.

Omoda also climbed into the trailing-3 top 20 for the first time, thanks to consistent sales of its E5 SUV.

Outlook

The UK ZEV mandate appears to be having the intended consequences, with the UK now pulling strongly ahead of France and Germany in EV share.

The UK’s broader macroeconomy is also marginally healthier than its neighbours, with 2025 Q1 YoY GDP hitting 1.3% growth (latest) on top of the 1.5% growth from Q4. Inflation marginally cooled to 3.4% in May from 3.5% in April. Interest rates remained at the new 4.25% rate set in early May. Manufacturing PMI improved again to 47.7 points in June, from 46.4 points in May.

What are you expecting from the transition in the UK? Where will EV share finish the year? Please share your thoughts and perspectives in the comments below.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Whether you have solar power or not, please complete our latest solar power survey.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy