June saw plugin EVs take 28.4% share in Germany, up from 19.8% year on year. BEV volumes were up modestly, while PHEVs increased strongly. Overall auto volume was 256,193 units, down some 14% YoY. The best-selling BEV in June was the Volkswagen ID.3.

The June auto market saw combined EVs take 28.4% share in Germany, with full electric vehicles (BEVs) at 18.4% share and plugin hybrids (PHEVs) at 10.0%. These compare with YoY figures of 19.8% combined, 14.6% BEV, and 5.2% PHEV.

The June auto market saw combined EVs take 28.4% share in Germany, with full electric vehicles (BEVs) at 18.4% share and plugin hybrids (PHEVs) at 10.0%. These compare with YoY figures of 19.8% combined, 14.6% BEV, and 5.2% PHEV.

Recall that the 2024 baseline was relatively weak for plugins, given the hangover from the sudden December 2023 BEV incentive cuts. Year to date, plugins now stand at 27.6% (and 17.7% BEV), compared to 18.6% (and 12.5% BEV) at this point last year. Germany is thus doing better than France, which is currently at a YTD cumulative share of 23.4% for plugins (and 17.6% for BEVs). Both are behind the UK, with a YTD plugin share of 31.8% (and 21.6% BEVs). Part of Germany’s growth in plugin share is due to the year-to-date overall market contracting by some 5% YoY. The same is true of France (down some 8% overall), but not the UK, where plugins are growing more strongly, despite the YTD overall market being up by 3.5% YoY.

The new Tesla Model Y is still not yet seeing big volumes in Germany, despite June being an end-of-quarter month. In June 2024, the Model Y registered 3,346 units, over 2,000 more than the June 2025 volume of just 1,304 units.

An even bigger YoY shortfall, however, was seen by the MG4 (registering just 609 units, a drop of 3,883 units YoY), and the Volkswagen ID.3 (registering 2,521 units, a drop of 3,849 units). At least in the case of Volkswagen, the new ID.7 has somewhat compensated, with YoY volume increase of 1,804 units. Cousins, the Skoda Elroq, Audi Q6 and Audi A6, have also helped make up for the ID.3’s YoY shortfall.

All of the new generation of small-and-affordable BEVs grew month-on-month, and added over 5,000 units YoY, from essentially nothing a year ago. More details on their progress below.

In terms of the overall evolution of the market, whilst plugin volume was up some 24% YoY, HEV and mild-hybrids were up by just 1% YoY, and combustion only vehicles were down by some 34% YoY.

Excluding December months, diesel-only share hit a record low of 13.9% in June, from 17.7% a year ago.

Best-Selling BEVs

Despite being down YoY (albeit from a very high baseline), the Volkswagen ID.3 nevertheless managed to narrowly secure the top spot in June, with 2,521 units. The new Skoda Enyaq secured second place, with 2,437 units. The Volkswagen ID.7 came in third, with 2,402 units.

It’s notable that June’s overall BEV volume was up by some 9% YoY, despite the top 3 seeing a combined volume of barely half that of June 2024’s top 3 (The ID.3, MG4 and Model Y).

This change reflects a broader strength in depth now, with the combined ranks 11th to 30th seeing a total of 11,715 units a year ago, and a much greater 16,468 units this time around. There are simply more good models to choose from now, many of which are selling decently well, at above 500 units per month. To quantify that, there are 34 models which sold >500 units this June, compared to 22 models at >500 a year ago.

Most of the moves in the top 20 were normal variations. Towards the bottom of the chart, however, was a notable new entrant, the BYD Dolphin Surf, with a healthy 817 units.

There were several new debutants in June. The highest volume was the MG S5, with 78 units. We’ve seen the MG S5 selling in other European markets for a few months already, and it is a decent value mid-sized SUV.

The new Peugeot e-408 also debuted, with 14 initial units. The e-408 is a D segment sedan with a length of 4,687 mm, and has a range of 453 km from its 58.3 kWh battery (decent efficiency). Its MSRP starts from €44,600 in Germany.

Also from Stellantis, the DS8 saw an initial 4 units in June, and the Citroën e-C5 Aircross saw 2 units. Unlike the Peugeot e-408, which is built on the older (multi-fuel) E-EMP2 platform, the DS8 and C5 are built on the newer BEV-focused STLA Medium platform. The DS8 is a D/E segment sedan (4,834 mm length) with an MSRP starting from €57,700. It will struggle against sedans from Mercedes, BMW, and Audi in Germany, not to mention the VW ID.7, but should do well in its home market of France.

The Citroën e-C5 Aircross is a C/D segment SUV with a length of 4,652 mm. It has battery options from 73 kWh to 98 kWh, and is priced from around €50,000 and up in Germany. This puts it right up against the Q4 e-tron, the BMW iX2, and similar vehicles, and I can’t help thinking that Citroën – just like the DS brand – will also struggle against the native German alternatives in this market.

The Hyundai Ioniq 9 debuted in June, with 6 units. A single unit of the new Nio Firefly was registered in June, but this is likely a testing unit for now.

In terms of the existing small-and-affordable models, the Hyundai Inster led the category with a record 1,325 units in June (ranking 9th in the overall BEV chart), up from 1,122 in May (ranking 10th). The Renault 5 registered 891 units, up from 406 in May (ranking 17th from 29th). The BYD Dolphin Surf saw a big increase, with 817 units in June, up from 38 units in May (ranking 19th from 84th).

Outside the top 20, the Opel Frontera saw 629 units in June, up from 401 (29th from 30th). The Dacia Spring saw 599 units, up from 202 in May (31st from 46th). The Leapmotor T03 saw 368 units in June, up from 297 in May (38th from 37th). The Citroën e-C3 saw 299 units, up from 279 (41st from 39th). The new Renault 4 increased to triple digits, with 207 units in June, up from just 7 units in May (47th from 111th). Finally the Fiat Grande Panda saw 50 units in June, up from 40 in May (80th from 83rd).

All of these affordable models are climbing, and together totalled 5,185 units in June, close to double their May sum of 2,792 units. I expect the Renault 4 to get close to the top 20 in the coming months, and perhaps the Citroën e-C3 Aircross may also do fairly well, once it arrives later in the year.

Notice that the Volkswagen group is still missing from this segment. Volkswagen brand plans to sell the ID.2 in 2026, and the ID.1 in 2027. Their cousin, the Skoda Equip, may also wait until 2026. Likewise, the Cupra Raval is expected in 2026. This slow-walking of affordability is a little disappointing, especially considering that the VW brand is meant to be “the people’s car”.

Here’s the trailing three month chart:

The Volkswagen ID.7 still leads, ahead of the ID.3, and the Skoda Elroq. Notice that Volkswagen Group models take all of the top 6 spots (as well as 8th, 9th, and 11th). The Tesla Model Y has now fallen to 13th (from 12th last month). A year ago the Model Y was in 5th spot, and in June 2023 it was the leader. Oh how the mighty have fallen.

The Volkswagen ID.7 still leads, ahead of the ID.3, and the Skoda Elroq. Notice that Volkswagen Group models take all of the top 6 spots (as well as 8th, 9th, and 11th). The Tesla Model Y has now fallen to 13th (from 12th last month). A year ago the Model Y was in 5th spot, and in June 2023 it was the leader. Oh how the mighty have fallen.

The Skoda Elroq is the most dramatic climber, now in 3rd, from 18th in Q1. The Hyundai Inster is the other big winner, climbing to 10th, from 23rd in Q1. The next model to watch is the BYD Dolphin Surf – on the current trajectory, it may enter the top 20 by the end of Q3.

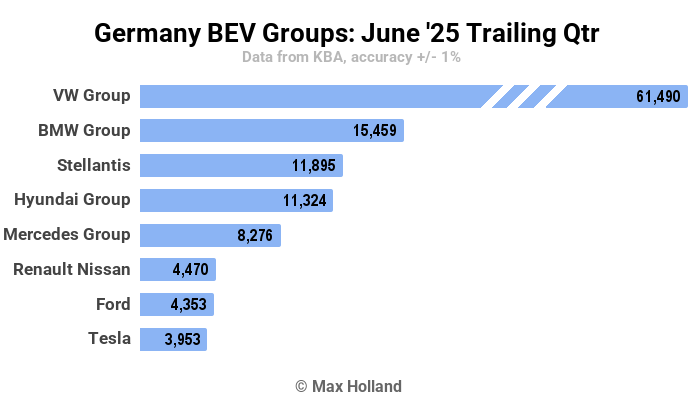

Let’s check in on the manufacturing group rankings:

Volkswagen Group still leads strongly, but its share dipped slightly to 45.6%, from 48.2% in Q1. BMW group remains in second spot, with share unchanged QoQ at 11.5%. Stellantis has grown share from 6.1% to 8.8% and stepped up from 5th to 3rd.

Other changes are just a shuffle of one place up or down, though Ford did well to climb from 10th to 7th, increasing share from 1.9% to 3.2%. Tesla is now in 8th, and less than 0.1% ahead of Geely, at 2.9% share. Just outside the chart in 10th, BYD climbed 2 spots, with share increasing from 0.9% to 2.7%. It would be a sign of the times if BYD managed to overtake Tesla by the end of Q3 – don’t bet against it.

Outlook

The 14% YoY fall in auto volume was significant, but may only be a blip from the softer YTD market contraction of 5%. Latest macroeconomic data remains that from Q1, with a flat YoY GDP tally, an improvement over Q4’s negative 0.2%.

Headline inflation moderated to 2.0% in June, from 2.1% in May. ECB interest rates dropped to 2.15% in early June, from 2.4% in May. Manufacturing PMI improved to 49.0 points in June, from 48.3 points in May. These macroeconomic figures are lacklustre at best, but an improvement over the past year and a half. The lowered interest rate might help prop up new car finance somewhat.

What are your thoughts on Germany’s EV transition? Is the fast growth of the small-and-affordable category something that will grow to make much difference to the transition rate overall? What new and upcoming models are you looking out for? Please share your thoughts and perspectives in the comments below.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Whether you have solar power or not, please complete our latest solar power survey.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy