EVs are picking up in Europe, with some 361,000 plugin vehicles being registered in Europe in June. That’s up 23% year over year (YoY).

This is a particularly positive sign when considering that the overall market (currently at ~6.8 million units YTD) does not look good this year (5% decline in June, -1% YTD).

Interestingly, while BEVs seem to be slowing down, growing just 16% YoY in June to 242,000 units, PHEVs are picking up the pace, jumping 40% YoY in June. They were spearheaded by the #3 BYD Seal U PHEV (aka euro-spec BYD Song PHEV), but other Chinese makes are also helping out, like Chery’s Jaecoo and Geely’s Lynk & Co. PHEVs scored close to 120,000 sales in June, and their YTD numbers are now up 24% to close to 600,000 units.

As such, June saw the plugin vehicle share of the overall European auto market grow to 29% (20% full electrics/BEVs), keeping the year-to-date numbers at 26% (18% for BEVs).

Comparing the EV best sellers in each size category with their respective ICE best sellers, one can see that there is still a lot to be done.

Generally speaking, the EV best seller in each size category is still far from reaching the overall podium, with the exception being the midsize category, where the Tesla Model Y reigns supreme. But even here, things looked better a few months ago when the Tesla Model 3 was 3rd.

Now that the US sedan is in decline (more on this down below), it’s been replaced on the podium by the Volvo XC60. The model is heavily electrified, with two out of three XC60 sales come from the PHEV version, but it is still better to have a 100% BEV model on the podium than a two-thirds PHEV.

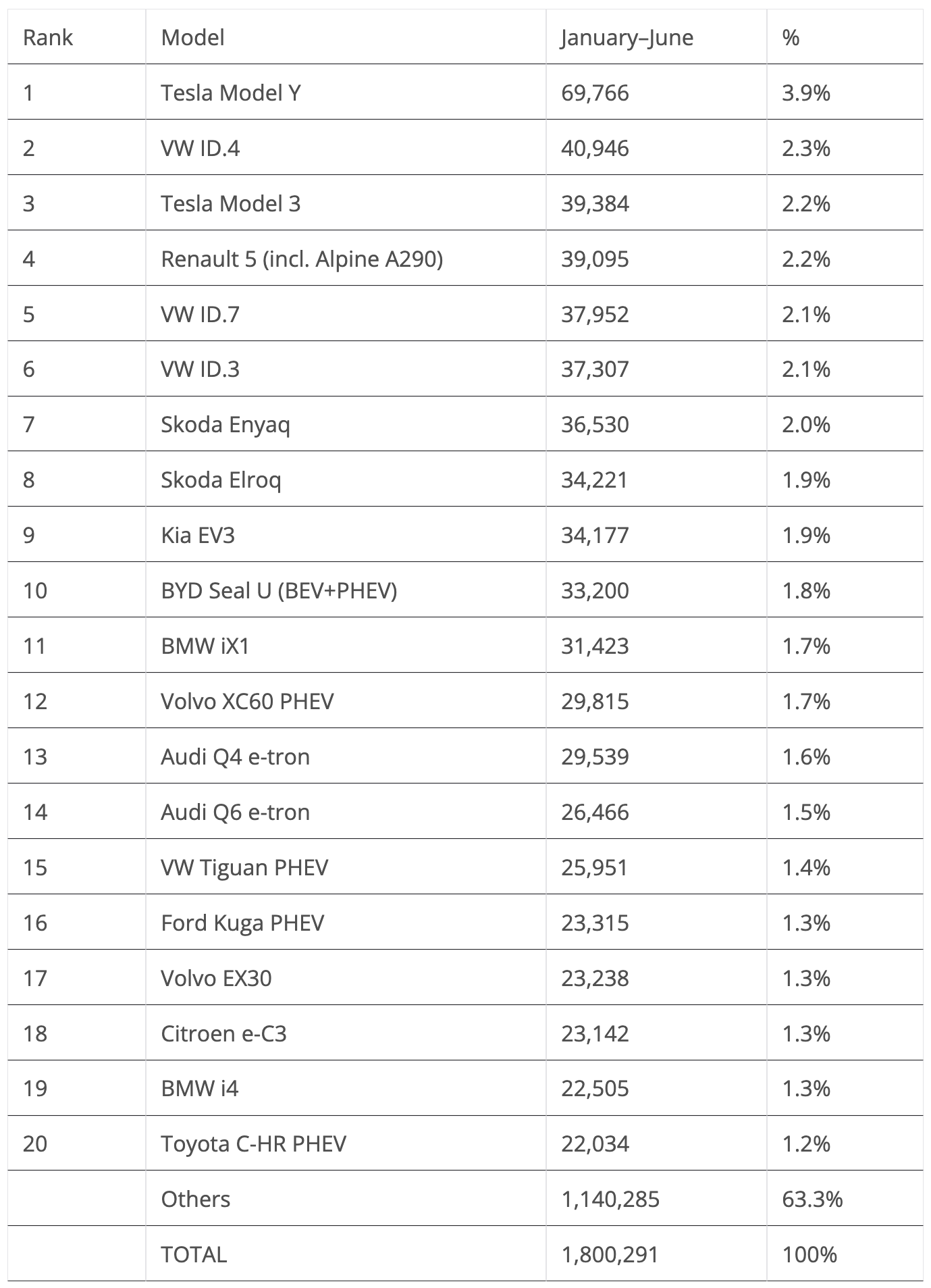

But let’s get back to June’s EV sales. The big highlight this month was Tesla’s #1 plus #2 win, maybe one of their last in Europe. Here’s a more detailed analysis on the top 5 EVs this month:

#1 Tesla Model Y — Tesla’s crossover retained its Best Seller status in June, thanks to 24,073 registrations. This is a slight 1% increase over its sales in June 2024. With the German-made EV profiting from its recent refresh, the crossover is looking to at least get close to its sales levels of 2023 and 2024. Considering all the hubris around the Texan brand, this result is welcome good news in a company where everything else seems to be falling apart…. Basically, Tesla is still floating thanks to the Model Y.

#2 Tesla Model 3 — The electric sedan scored 10,807 registrations in June. That represented exponential growth month over month (MoM), but a horrible 48% drop YoY. With the brand focussing on the refreshed Model Y, which is benefitting from higher discounts than its sedan sibling(!), and developments of new versions, like the Tesla Model Y L and a more decontented and cheaper version*, the Model 3 is being left out in the cold. This means that the sedan should continue to lose sales and podium presences will become more rare.

* My name suggestion for this cheaper and more spartan version of the crossover is the Tesla Model Y Leonidas. You are welcome, Tesla….

#3 Skoda Elroq — The recently introduced Elroq scored another record performance, 9,825 registrations in June. Will we see it go north of the 10,000-unit mark in September? Volkswagen Group has struck gold with this one. Despite minimum effort (basically, it slightly shortened its successful Enyaq), Skoda won a top three presence AND did it without significantly hurting the Enyaq’s sales. The longer crossover actually increased its sales by 8% YoY in June. Although not as spacious as its bigger sibling, it compensates for that with a competitive price, starting at 34,000 euros, which makes it one of the cheapest compact crossovers on the market, Chinese included. Could this be the new value-for-money king? This great performance allowed Skoda to score some 16,000 BEVs in June, a great result for the Czech brand.

#4 Renault 5 / Alpine A290 — The sporty hatchbacks won another top 5 presence in June, with the French duo scoring 7,788 deliveries. The EV enthusiasts’ choice, for a number of reasons, starting with its dropdead gorgeous looks and ending in the hot hatch–like handling, the 5/A290 has enough going for it to attract a wide audience, even if it is not as wide as their ICE siblings, the Renault Clio and Dacia Sandero. Then again, that’s not their responsibility, as both the Sandero and Clio will receive their own EV versions a couple of years from now.

#5 BYD Seal U (BEV+PHEV) — BYD’s star player delivered a record 7,182 sales (720 of them being of the BEV variety), with the model staying on the best sellers list in Europe. While the Seal U, the euro-spec version of the veteran Song, isn’t class leading specs-wise, it compensates for that with competitive pricing, which is especially appealing in the PHEV version that starts just below 40,000 euros, a killer price for a midsize SUV. Just for an idea, the value-for-money minded Skoda Kodiaq midsize SUV starts at 45,000 euros, with a 1.5 MHEV engine and 150 hp, while the cheapest Seal U PHEV costs 5,000 euros less, is more powerful, has a combined power of 217 hp, AND, as a cherry on top, still offers 80 km of electric WLTP range. Not bad, eh?

Outside the top 5, the highlight comes from Volkswagen, which saw the new Tiguan PHEV beat the Volvo XC60 PHEV and take the plugin hybrid category title, thanks to a record 5,234 units. With over 100 km electric range, and DC charging, the German crossover specs make it a decent PHEV effort, so I wouldn’t be surprised if it started to win the category title more often.

Another model shining was the #8 BMW iX1. With 6,499 sales, it had its best result in 18 months, comfortably outselling its direct rivals, the #19 Mercedes EQA and #13 Audi Q4.

Outside the top 20, the big highlights were the Polestar 4 hitting a record 2,966 units, helping the Sino-Swedish brand to get much needed sales volumes, and the VW ID.Buzz scoring another record performance, 2,757 sales.

Speaking of VW’s neo-retro Hippy Van, the German-made EV is helping MPVs to have something of a resurgence. This family-friendly vehicle category is seeing its sales jump 99% YoY this year, well above the 24% average, allowing MPVs to have 3% of the market. Sure, it is still a small portion of the market, but sales are going in the right direction. MPV segment growth beat almost every other vehicle category, with the exception being the even more niche sports cars/coupés/convertibles category, which we could call Sports Specialties. That segment grew 209% YoY, gaining a grand total share of … 0.3%.

Still, these are necessary steps to help the EV market to become more diversified and less stereotypically crossover-heavy.

And as I have been saying for years — MPVs will rise again!… [Editor’s note: Knowing José for about 10 years, I can confirm that he has been on this bandwagon for a long time, and his heart is fully in it. —Zach]

Looking at the 2025 ranking, there were plenty of changes. The Tesla Model 3 had its expected end-of-quarter surge, but this time it wasn’t enough to recover the #2 spot from the VW ID.4, giving strength to the idea that, after three (2022/23/24) consecutive #1 plus #2 wins by Tesla in the model table in Europe, 2025 will be the year that this kind of domination will start to fade.

Even the 3rd spot is all but guaranteed for the Tesla sedan, as plenty of models (Renault 5, VW ID.7 & ID.3…) are dangerously close and could surpass it. The rising #8 Skoda Elroq could especially become an adversary too strong to contain in Q4.

And with the Tesla Model 3 in a seemingly downward spiral (it is down 35% YoY this year, while in June it fell by 48% YoY), 2015 could see the US sedan stay below the European EV podium for the first time since 2018!

The remaining changes allowed the #15 VW Tiguan PHEV, #16 Ford Kuga PHEV, and #17 Volvo EX30 to climb a position each, benefitting from another disappointing performance from the Citroen e-C3.

Finally, the BMW i4 surpassed the Toyota C-HR PHEV and is now #19, with the Japanese crossover now feeling the heat from the #21 Cupra Born, which is only some 200 units behind.

Looking at the plugin auto brand ranking, this time the leader, Volkswagen, has lost share (11.2% in June vs. 11.5% in May), but it still holds a comfortable 2.2% share lead over #2 BMW.

This means that the German make is on its way to finishing a three-year Tesla reign (2022/23/24) in Europe, winning its first manufacturer title since 2021.

Speaking of Tesla, the Texan automaker profited from its end-of-quarter push, raising its share by 0.9% from 5.2% to 6.1%, and thus climbing into … 4th. Not bad, but … we are talking about the trophy holder. Tesla’s 2024 title was its 3rd in a row. And now it is fighting for a spot in the top 5.

The end of an era?

Below the top 5, growing #7 Skoda rose from 5% in May to its current 5.1% share. The Czech brand is probably the best candidate for a top 5 presence, and also a welcome addition to the table, as Volkswagen is the single mainstream brand in the top 5, followed by four premium makes.

Having Skoda on the best sellers table will be a good sign of EVs going mainstream. Fingers crossed….

A deserving mention also goes to BYD, which is already appearing on the radar with 4.1% share, a 0.1% increase over May.

Arranging things by automotive group, Volkswagen Group is firmly in the lead, despite losing 0.3% share in June. It is now at 27.8% share, a market share that is comparable to BYD’s in China and Tesla’s in the USA. This is an important metric for the German conglomerate if it wants to stay relevant in a fully electrified global automotive market.

If you can’t win at home….

BMW Group (10.5%, down from 10.6% in May) remained in the runner-up position in June, while #3 Stellantis is in its long hard road to hell (9.2% in June vs. 9.5% in May). With too many brands and too little money to develop them, maybe it would be good to sell a couple of them? Say, Lancia and Maserati? Both storied makes need attention and lots of money in order for them to develop and flourish, and right now, these two items are in short supply at Stellantis….

And do something about DS. Either reintegrate it into Citroen, or make it a proper premium brand. But for that, you will need patience and money. After all, making a successful French premium brand is something for decades, not years. Just look at what Renault is doing with Alpine.

But back to the top 5, Hyundai–Kia (7.9%, down from 8.1% in May) remained in 4th, but has seen Geely (7.8%, up 0.1%) get closer, and might threaten the Korean’s 4th position.

Despite seeing Volvo lose sales, Lynk & Co, Zeekr, and Polestar are compensating for the Swedish brand’s falling sales, thus keeping Geely on a growth path.

Finally, a note on the recent USA-EU tariff agreement.

Regarding EVs, it’s not as bad as it seems. Here’s how it works:

- The EU didn’t want to impose tariffs on US-made cars because the biggest US exporters to the EU are … German brands. (BMW X5, Mercedes GLE, etc. are made in the US and exported here.) So it didn’t make sense to do that.

- Regarding Tesla, things won’t change much. The Model Y is already made here in Germany. The Model 3 is cheaper to make in China than in the US, even with the tariffs on China as they stand.

- Regarding the Cybertruck and Semi, the most important question isn’t the tariff or the price, but the regulations, which are different here in Europe. Thus, this difference in tariffs doesn’t make much difference to the viability of selling both in Europe.

- The Model S and X could see their prices reduced, but it doesn’t solve their main problem: they are models that are more than 10 years old, and as such, not very competitive.

In conclusion, there will be a little more competition at the top end of the market, but the rest will be the same.

As for US buyers, there will be less choice. Cheaper models will probably be canceled, and the ones that stay will cost more. Still, most best selling European models in the USA are already made there, so … it’s not as bad as it seems.

And I am talking about the EV niche. Regarding the larger agreement, I am not an expert on trade, but personally, both options (going to a trade war or trying to reach an agreement) were worse than what was there before. You can choose one or the other; I’m not a politician, so I don’t have to choose. 😄

But have no doubt, neither of the two options are better than what was there before. Whoever says otherwise either doesn’t know, or is a politician looking for easy votes.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy