July’s auto sales saw plugin EVs take 24.0% share in France, up from 20.8% year-on-year. BEVs grew share, whilst PHEV remained flat. Overall auto volume was 116,350 units, down some 8% YoY. The Renault 5 was the best-selling BEV for the month.

July’s auto sales totals saw combined plugin EVs take 24.0% share in France, with 16.8% full battery-electrics (BEVs) and 7.2% plugin hybrids (PHEVs). These compare with YoY figures of 20.8% combined, 13.5% BEV, and 7.3% PHEV.

The year-on-year baseline comparison was skewed by a slow period in 2024 between the end of new “social leasing” signings and the arrival of the Citroen e-C3 and the Renault 5 in the Autumn. So, whilst the YoY uptick appears positive, the baseline was in fact abnormally low. More generally, the plugin market share has barely risen since late 2023, as the below powertrain timeline graph clearly shows.

The more notable trend has been the replacement of ICE-only sales with non-plugin hybrids (HEVs and MHEVs), represented by the rapidly growing blue segment in the graph below. This demonstrates that legacy auto companies are generally taking a “lowest hanging fruit” approach to meeting emissions requirements, rather than going all in on plugins, and especially on BEVs.

Nevertheless, with more affordable BEVs like the new Renault 5 and Citroen e-C3 regularly seeing strong volumes recently, and the Hyundai Inster debuting in July, with the BYD Dolphin Surf about to make first customer deliveries, plugin share may soon improve in France.

Best Selling BEV Models

The Renault 5 was once again the best selling BEV in July, with 2,033 units, its fourth time in the top spot this year (and never out of the top two). In second place was the BMW iX1, with a personal best 1,084 units. In third was the Tesla Model Y, with 979 units.

July volumes were fairly weak overall, with the BMW iX1 being the only member of the top 10 seeing growth over recent averages – thus its strong ascent to second place. However, this is an established seasonal pattern, with July and August often the slowest months of the French auto market.

Further back, the new Renault 4 maintained its 12th position from June, and can surely climb higher.

There was one important debutant in July, the new Hyundai Inster, which landed in 17th place, with 336 initial units. There’s every reason to expect the Inster to quickly climb to over 500 units per month and start competing with the domestic small-and-affordable competition.

We don’t yet have visibility on what’s happening with the new BYD Dolphin Surf in France, beyond the generous 414 showroom units which arrived in May. The Surf is already selling hundreds of monthly units in each of the large neighbouring markets of Germany, Italy, Spain (where it ranked 2nd in July), and the UK. Let’s watch out for its move to customer deliveries in France.

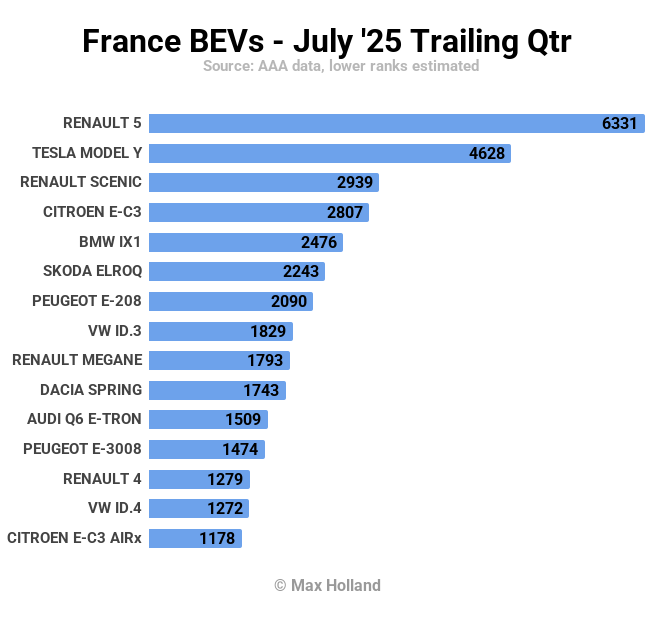

There’s no great surprise about the top two spots in the trailing 3-month rankings. The Renault 5 is of course leading, with 6,331 units. After a strong June, the Tesla Model Y (with 4,628 units) is safely in second place, well ahead of the third placed Renault Scenic (2,939 units).

The Renault 4 is now firmly in the mid-rankings (13th), and we can expect it to enter the top 10 at some point, once production volume is ramped. The Citroen e-C3 Aircross is still visible only by virtue of its strong May, having seen much weaker volumes in June and July.

How long before the Hyundai Inster makes it into the above chart? I would guess perhaps sometime in Q4.

Outlook

July was the 15th consecutive month of falling YoY volume in the French auto market, with December 2024 being the only exception (and even that was effectively flat YoY).

The broader macroeconomy is consistent with this trend, with latest Q2 2025 data showing 0.7% YoY GDP growth, maintaining the weakness seen in Q1, and Q4 2024.

Headline inflation was steady at 1% in July (from a revised-up 1% in June). ECB interest rates have remained at 2.15% since early June. Manufacturing PMI barely shifted, at 48.2 points in July, from 48.1 points in June.

What’s next for the French auto market? When might we see BEV growth resume? What BEV models are needed and at what price points? Please jump in below with your thoughts and perspectives, and join the conversation.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy